Selecta. Going Long SSNs At 95.375 (7.2% YTW) & Selling 5y CDS At 474bps

03 March 2020

high-yield

Selecta. Going Long SSNs At 95.375 (7.2% YTW) & Selling 5y CDS At 474bps

Massimiliano Zanetti Bottarelli & Rupesh Tailor, Everest Research, 3 March 2020

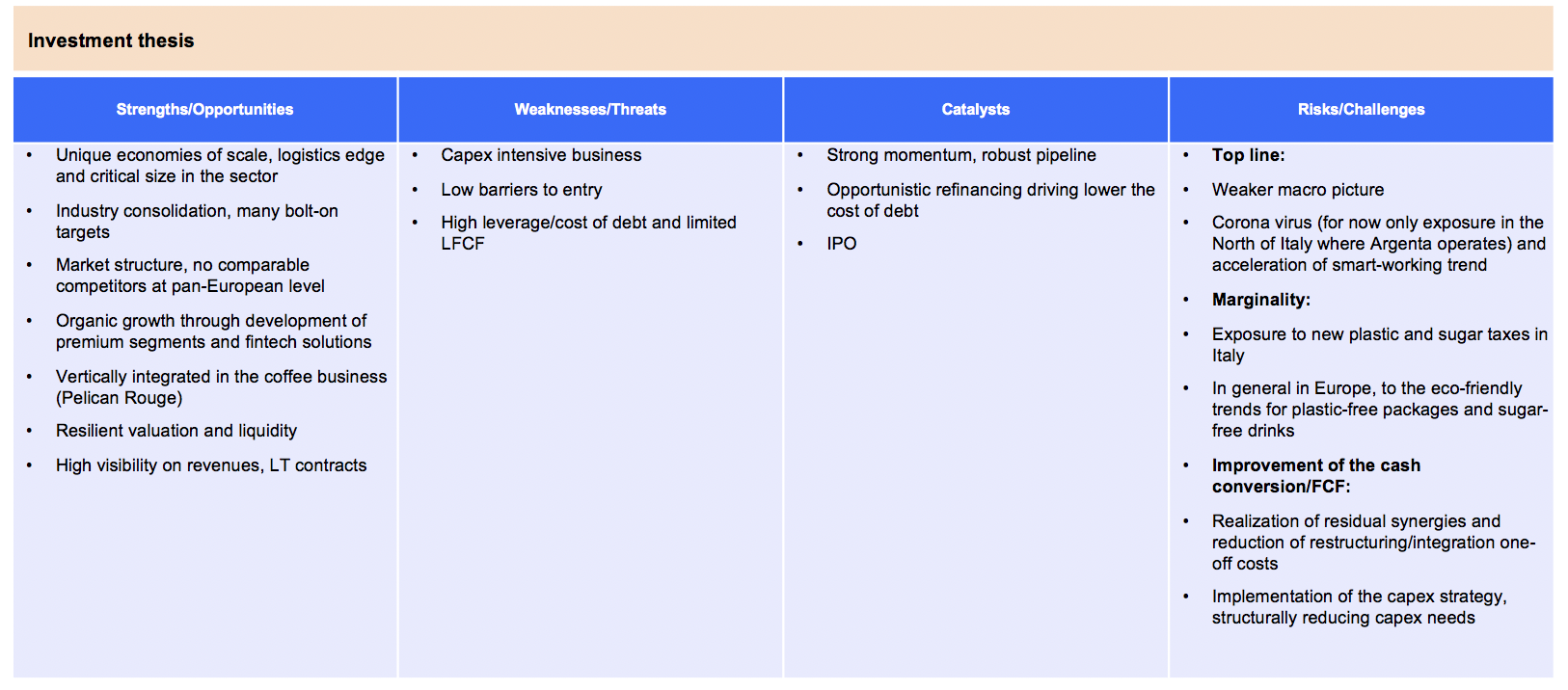

- We published a deep dive last week on Selecta, the European unattended self-service retail market leader, and now see an attractive opportunity to go long risk via both the Senior Secured Notes (SSNs) and 5 year CDS. See our initiation Memo for more detail

- Selecta’s Senior Secured Notes (SSNs) and CDS recent spread widening reflects the uncertainty around the extent and duration of its exposure to coronavirus (COVID-19) which will likely result in lower sales due to fewer hours worked at the office and lower footfall in public locations where Selecta’s PoS are located

- Absent a severe escalation of the epidemic in Europe, we believe Selecta will register only a slight negative impact in Q1 20, potentially continuing for several quarters. We view Selecta’s liquidity profile as robust and sufficient to withstand a prolonged crisis. The coronavirus impact on the unattended self-service retail sector could even turn out to be an opportunity in terms of increased potential for bolt-on acquisitions on favourable terms of the most exposed and weakest players

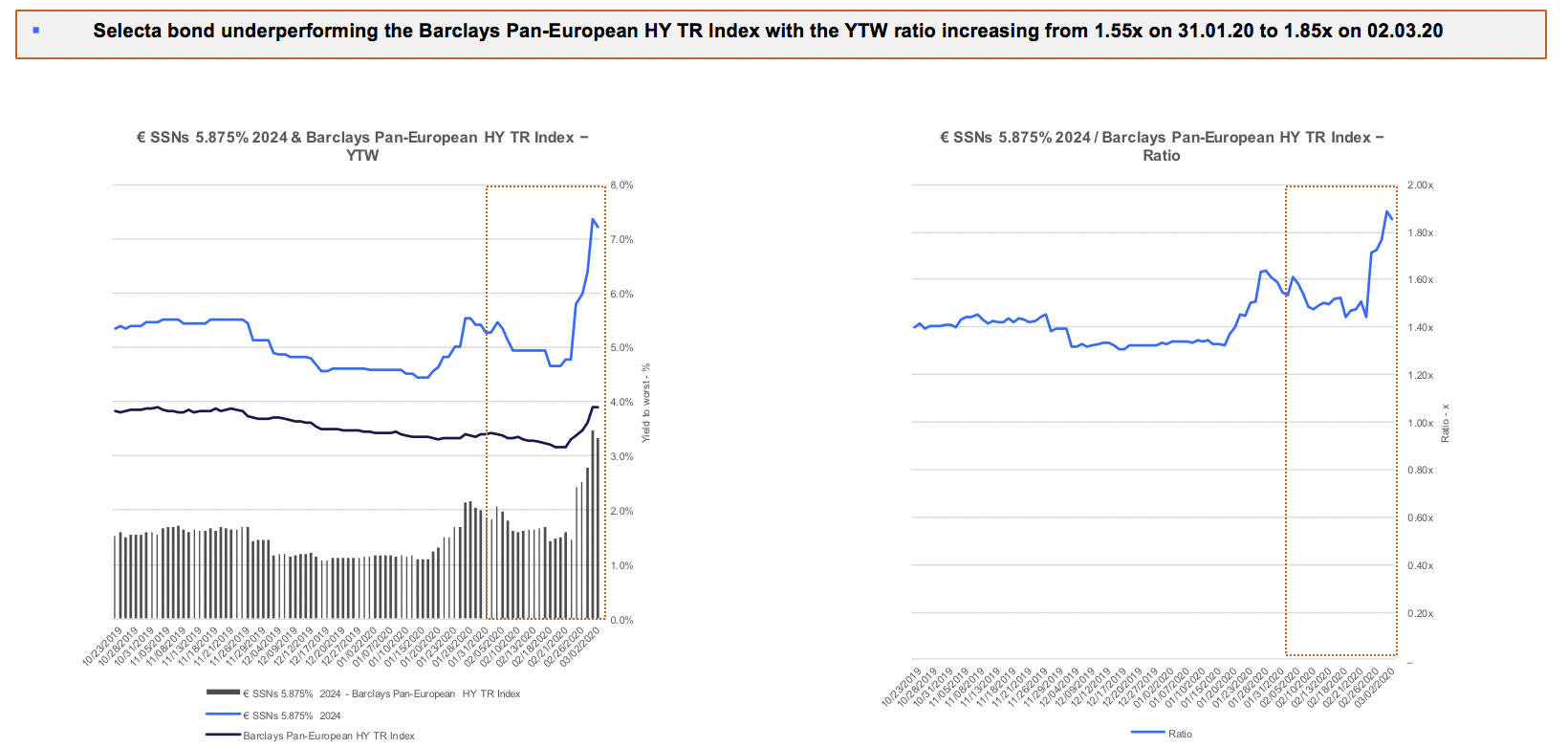

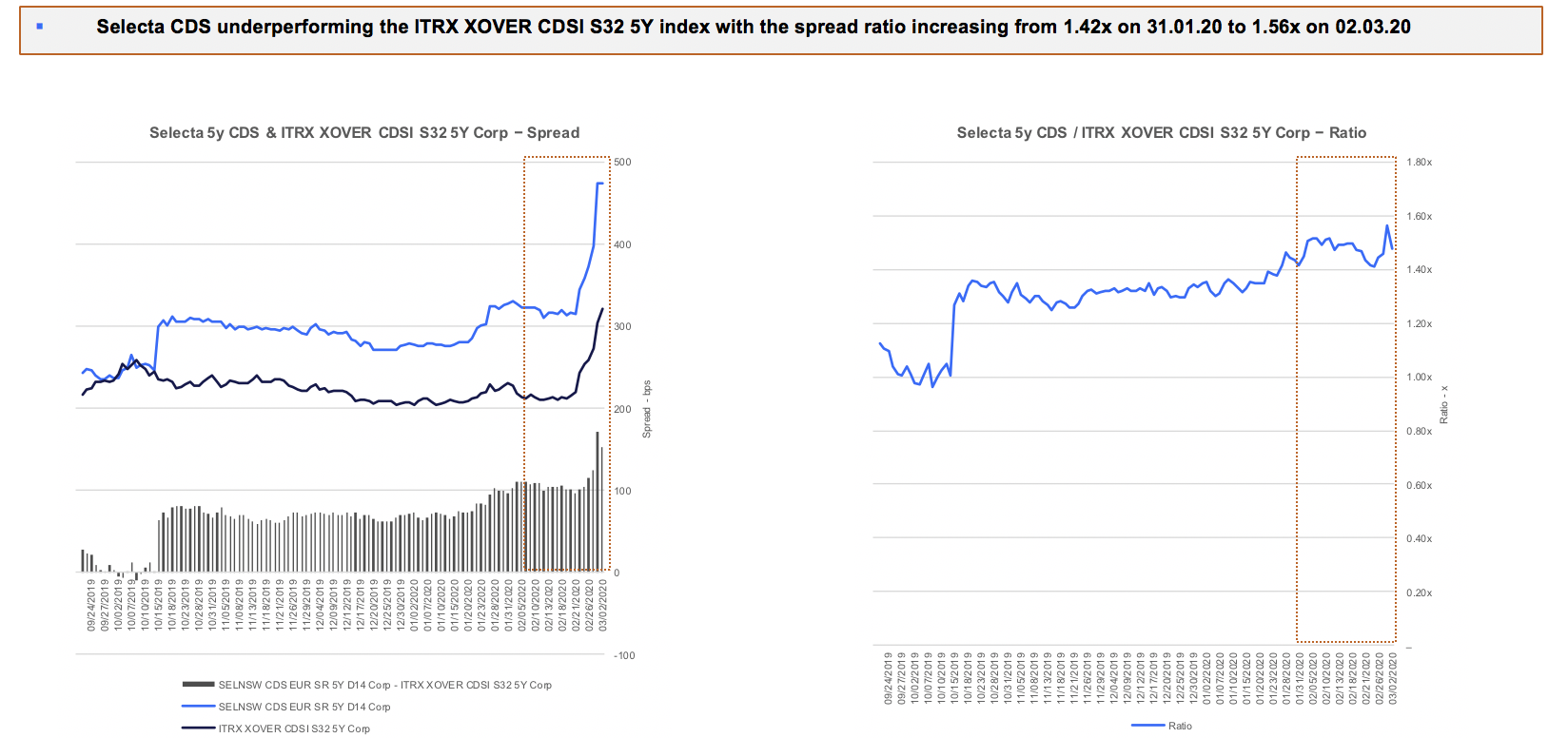

- In relative terms, Selecta’s CDS and SSNs slightly underperformed the relevant benchmarks across CDS and cash markets respectively over the past week. Even with the refinancing and IPO window closed in the short-term, which could have represented an exit for current bondholders, in absolute terms we think the market is not appreciating Selecta’s resilient business and valuation even in our bear case scenario (which does not include a COVID-19 epidemic) which shows 100% recovery on SSNs

- Following our Avoid recommendation on 26.02.20 on both the SSNs at a price of 100.125 and on the 5 year CDS at a spread of c. 345bps, we now move to Buy on the SSNs and “take” a new 2% long “position” in our model “portfolio” in Selecta’s € SSNs 5.875% 2024 at a price of 95.375 (good upside to the call at c. 103 if markets re-open). We move to a Sell recommendation (i.e. long risk) on Selecta 5 year CDS and “sell” Selecta 5 year CDS for 2% of model portfolio AUM at a spread of c. 474bps, motivated by the higher upside potential offered by selling CDS (as compared to buying SSNs) in the event that a CDS orphaning arises following an IPO as per our initiation Memo

- Close on 2/3/20

Contact Rupesh Tailor at Everest Research to discuss: [email protected]

Everest Research - Deep dive high yield research, distressed debt research and independent equity research