Thomas Cook – c. £1.9bn Base Case Break-Up Enterprise Value

10 June 2019

high-yield

Thomas Cook - c. £1.9bn Base Case Break-Up Enterprise Valuation

Rupesh Tailor, Everest Research, 10 June 2019

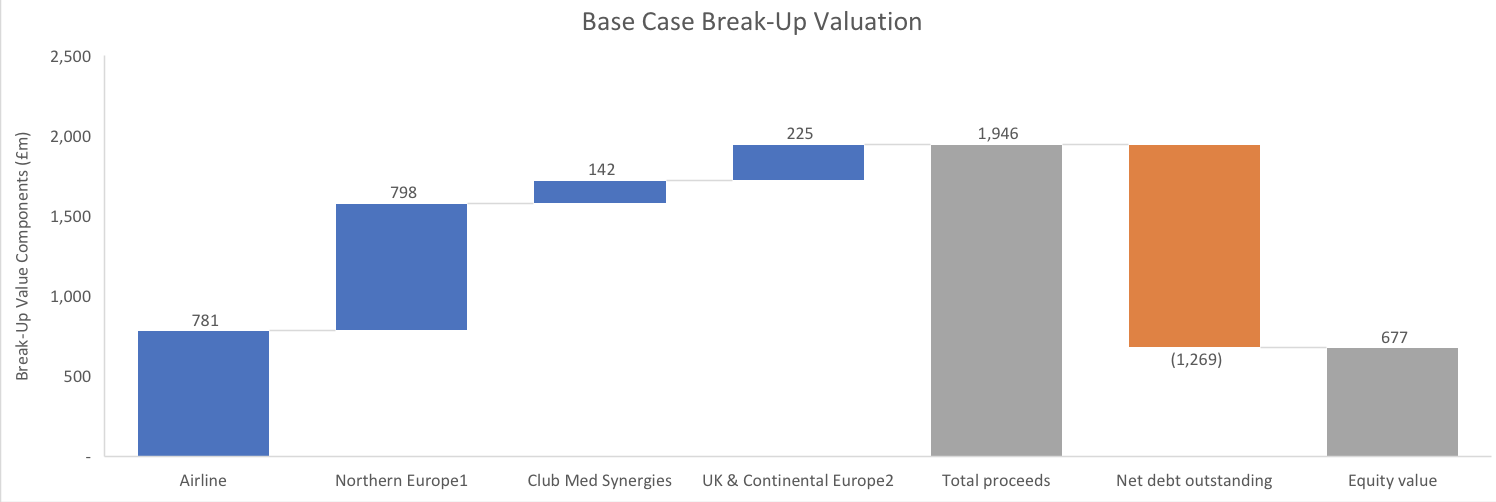

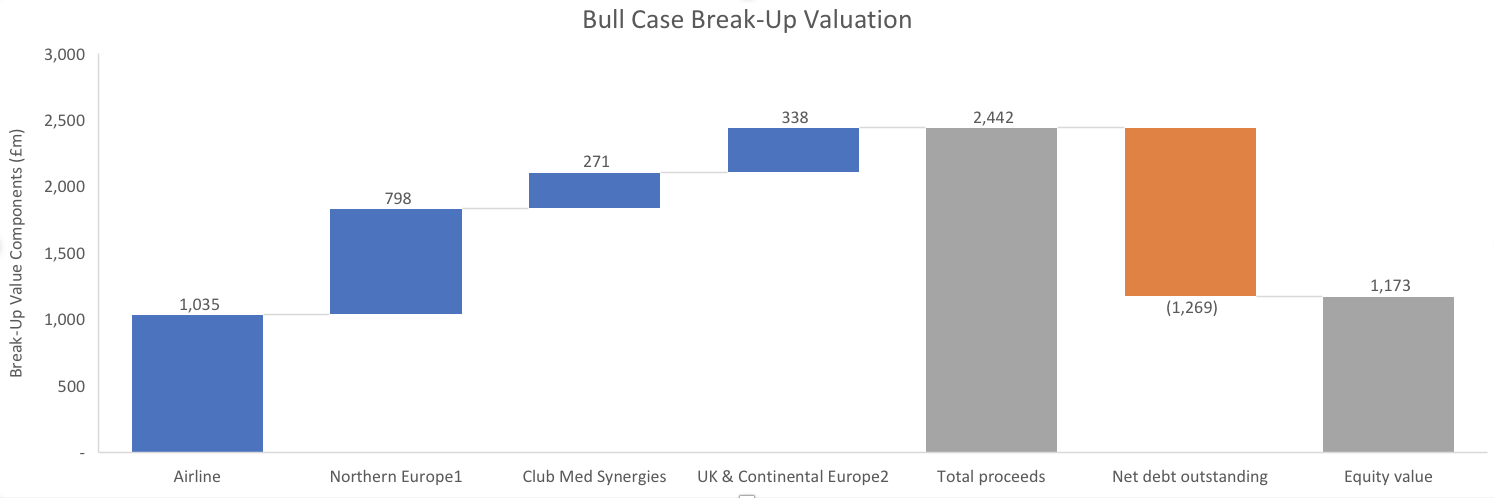

- As per our note from last week, we see a going-concern break-up of Thomas Cook as more likely than a near term administration or CVA. Our base case break-up enterprise valuation (see/expand charts below) of Thomas Cook comes out at c. £1.9bn, leaving £677m equity value or £0.44 per share compared to the current share price at c. £0.19 per share. Our bull case break-up enterprise valuation is at c. £2.4bn, valuing the shares at c. £0.76 per share

- Specifically, we see a break-up into all or some of the following constituent parts (some of which may themselves be broken up further): (1) the Group Airline (potentially excluding Thomas Cook Airlines Scandinavia A/S); (2) the Northern European business (both the tour operator and airline businesses), for which private equity firm Triton has submitted a bid; and (3) the remaining UK and Continental Europe tour operator businesses (Fosun is in discussions currently to acquire the Group Tour Operator business)

- We have valued the synergies between Fosun's Club Med business and Thomas Cook's Group Tour Operator business based on Thomas Cook's distribution capability increasing Club Med's occupancy rate to (eventually) 72% (from 66% in 2018) in our base case and to (eventually) 78% in our bull case and the resulting increase in our DCF valuation of Fosun Tourism Group's (FTG) Club Med business (which FTG reports under as its "Resorts" segment)

- As per our note, other top European sun and beach hotel operators are able to achieve occupancy rates of up to high 80%s even over a full year, e.g. Tui's Riu hotels achieved 89% occupancy over FY 2018. However, 19% of Club Med's capacity (as measured by number of beds) comes from "Mountain" resorts which are essentially ski resorts and, in our view, will always be constrained in the full year occupancy rate they can achieve. 78% in our bull case represents our view as to the maximum occupancy rate Club Med can achieve over a full year given its mix of resorts across "Sun" and "Mountain" categories. We assume in our Thomas Cook break-up values below that Fosun "pays" 50% of the synergies to Thomas Cook through the price it may pay for Thomas Cook's Group Tour Operator. The full synergies we estimate for FTG's Club Med business are £284m in our base case and £543m in our bull case

- For more details on the Club Med / Thomas Cook combination rationale and our valuation of the other parts of the Thomas Cook Group, please see our note from last week

- "Northern Europe" refers here to both Thomas Cook's Northern European tour operator and airline businesses. Consequently, "Airline" in the charts refers to the Group Tour Operator excluding Thomas Cook's Scandinavian airline

- "UK and Continental Europe" in the charts refers only to Thomas Cook's UK and Continental European tour operator business, excluding its UK and German airline businesses

Contact Rupesh Tailor at Everest Research to discuss: [email protected]

Everest Research - Deep dive high yield research, distressed debt research and independent equity research